|

Riverside Bankruptcy Attorney - Expert Personal and Corporate Bankruptcy Lawyers serving Riverside, California. If you are struggling financially and looking to speak with a Riverside bankruptcy attorney, you've come to the right place. The Attorney Group can help you eliminate your credit card debt, pay day loans, personal loans, medical bills and other bills and debt. We will stop lawsuits, stop garnishments, stop, bank account levies, stop judgments and stop foreclosures. We have 36 locations to meet you in California.

Need immediate assistance? Contact us now!

Toll Free 1(888) 754-9877 Available 7 Days a Week 7am to 9pm 36 LOCATIONS IN CALIFORNIA

A bankruptcy is an opportunity for many debtors to be relieved of constant harassing phone calls from creditors and collection agencies, the threat of lawsuits, levies, seizures and impending foreclosure. Though you should definitely explore other options to getting your debt under control, consulting with a bankruptcy attorney to see if a bankruptcy might be your best option, to determine if you qualify for relief and which chapter is appropriate based on your particular circumstances is essential. There are many misconceptions regarding bankruptcy. As a consumer or small business owner, you have the option of a Chapter 7 liquidation or a Chapter 13 reorganization. Chapter 7 Liquidation Chapter 7 can be utilized by individuals, married couples, businesses and corporations. It is a liquidation of your debts and possible relinquishment of certain assets if found to be nonexempt. In most consumer and small business cases, however, you are able to retain most if not all of your personal assets. Also, filing automatically stays or stops all collection activities. You do have to qualify for a Chapter 7 proceeding if your debts are primarily consumer and not business by proving that your income is low enough so that you cannot pay your debts. Your monthly income must be lower than the median income for your state. In California, the median income for a single individual is $47,798 and for two, $62,009. Otherwise, your disposable income must be low enough to qualify. This is determined by deducting your monthly expenses from your average monthly income over the past 6 months. If it is too high, you may still consider a Chapter 13 petition. In any bankruptcy, you must list all of your debts, regardless if you plan on repaying a certain debt or not. You must also have not transferred any substantial property within 90 days of filing or within one year if such transfer was made to a relative or business partner or the court can void it. A list of your monthly expenses and assets is also required. You are entitled to certain exemptions regarding your personal assets so that the trustee will not seize them for the benefit of your creditors. For example, you can exempt a motor vehicle, much if not all of your home equity, retirement accounts, bank accounts, furniture, tools of your trade and other items. Consult with our expert bankruptcy lawyer about what exemptions are available to you. You must also take an approved credit counseling class before filing and a personal financial management class before your discharge. Most discharges occur about 4 months after you file. Your unsecured debts, such as credit cards and medical expenses, are dischargeable. Chapter 13 Reorganization If your disposable income is too high, or if you wish to continue operating your small business, or you face foreclosure of your home, then a Chapter 13 is an option. You must have a steady income, though, so that your debts, to some degree, are paid within either a 3 or 5 year plan. There are limits to the amount of secured and unsecured debt you have. Consult with your attorney if your debt is unusually high. The length of your repayment plan depends on your income. If it exceeds the state’s median, your plan will likely be 5 years. A chapter 13 can save your home from foreclosure provided you can make your regular monthly mortgage payments while repaying your arrearages over the life of the plan. Any second mortgage would be discharged at the termination of the plan if all is otherwise successful. Further, you can have past due taxes, student loans and child support payments paid off within the plan as well. Bankruptcy protection might be the relief you are seeking. Consult with an experienced bankruptcy attorney about your particular circumstances and to see if filing for bankruptcy is the right decision for you. |

Keep Your CAR

Keep Your HOUSE

Keep Your DIGNITY

Keep Your RETIREMENT

Keep Your 401K

Keep Your PENSION

20

Years Experience

9,800+

Happy Ch 7 Clients

EVICTION

Bankruptcy . Criminal

36 Locations

In California

800+ 5 Stars

Combined Reviews

PHONE

Start your case by phone

$100 Million

Discharged

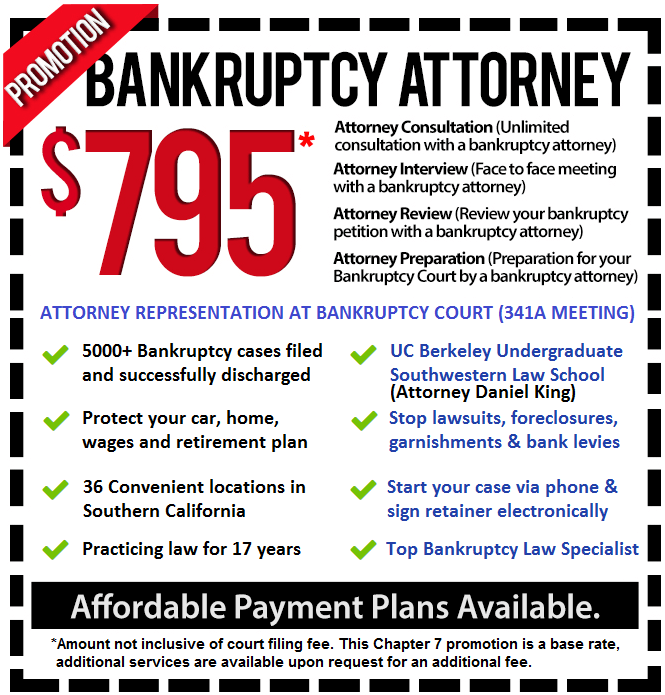

Daniel J King, Esq.

Managing Attorney/Owner

UC BERKELEY

Undergraduate

SOUTHWESTERN

Law School |

|

Free Consultation

100% Free Consultation

(Today)

Process Petition

Become a client

Run Credit Report

Process Petition

Review/Amend Petition

Attorney Meeting

Review Petition

Confirm Petition

Prepare for BK Court

Freedom

341a Meeting of Creditors

(Bankruptcy Court)

with Bankruptcy Attorney

Attorney Daniel J King

Education: UC Berkeley UndergraduateSouthwestern University School of Law

$100,000,000+

Debt and Taxes Discharged

| 19 | 7,500+ |

| Years Experience | Happy Clients |

Need Help? Call: 1-888-754-9877

The information on this website is for general information purposes only. Nothing on this site should be taken as legal advice for any individual case or situation. This information on this website is not intended to create, and receipt or viewing of this information does not constitute, an attorney-client relationship.

LOCATION DISCLAIMER: The Attorney Group has a main office in Anaheim Hills, California. All other addresses are local offices available on an advanced appointment basis for meetings and depositions.